Note

Click here to download the full example code

ARMA model

The moving average

The code below simulates the moving average model.

import random

import numpy as np

import matplotlib.pyplot as plt

import matplotlib

from pylab import rcParams

matplotlib.font_manager.FontProperties(family='Helvetica',size=11)

rcParams['figure.figsize'] = 14/2.54, 14/2.54

def plotOverTime(ax, w):

n=len(w)

t=np.arange(n)

ax.plot(t,w, '-',color='k')

ax.set_xlabel('Time: t')

ax.spines['top'].set_visible(False)

ax.spines['right'].set_visible(False)

ax.set_xticks(np.arange(0,n,step=n/5))

ax.set_yticks(np.arange(-n,n+1,step=10))

ax.set_xlim(0,n)

ax.set_ylim(-2*np.sqrt(n),2*np.sqrt(n))

def MA(w0,steps,c_vals,sigma=1):

# n step random walk

w = w0

w_k = np.zeros(steps)

#The random values can be produced in advance

e_k = np.random.normal(0, 1,steps)

for k in range(steps):

w_k[k]= w

#Add the most recent value

w = e_k[k]

#Add the weighted average of older values

for j,c in enumerate(c_vals):

w += c*e_k[k-j-1]

return w_k

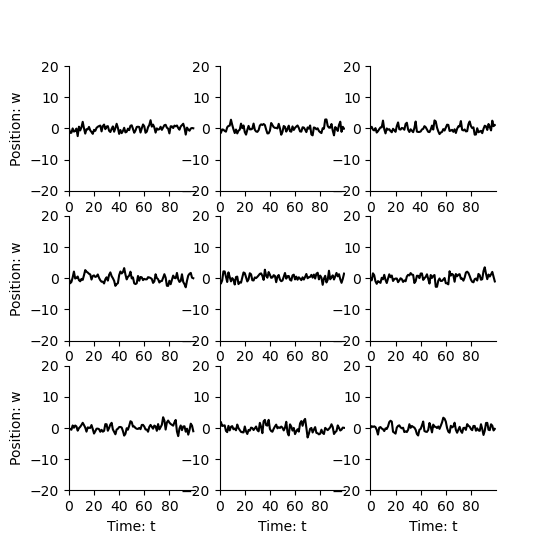

fig,axs=plt.subplots(3,3)

steps=100

for axsr in axs:

for j,ax in enumerate(axsr):

w=MA(0,steps,[0.5])

plotOverTime(ax, w)

if j==0:

ax.set_ylabel('Position: w')

This process doesn’t move far from zero, because it has no “memory”.

Autogressive model

Here we plot the AR(1) model with :math;´a_1=-0.9´.

def AR(w0,steps,a_vals,sigma=1):

# n step random walk

n=len(w0)

#Setup intial conditions

w_k = np.zeros(steps)

w_k[0:n-1] = w0

#The random values can be produced in advance

e_k = np.random.normal(0, 1,steps)

for k in range(n,steps):

#Add the noise

w = e_k[k]

#Add the weighted average of older values

for j,a in enumerate(a_vals):

w += -a*w_k[k-j-1]

w_k[k]= w

return w_k

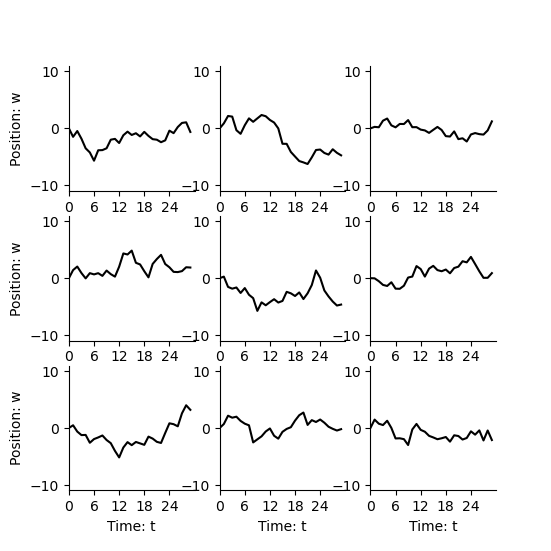

fig,axs=plt.subplots(3,3)

steps=30

a_vals = [-0.9]

for axsr in axs:

for j,ax in enumerate(axsr):

w=AR([0],steps,a_vals)

plotOverTime(ax, w)

if j==0:

ax.set_ylabel('Position: w')

Now there is a longer memory. The process increases and decreases more slowly in comparison to the fluctuations caused by noise.

When we reduce :math;´a_1´ then the process moves more randomly, like the random walk.

fig,axs=plt.subplots(3,3)

steps=30

a_vals = [-0.1]

for axsr in axs:

for j,ax in enumerate(axsr):

w=AR([0],steps,a_vals)

plotOverTime(ax, w)

if j==0:

ax.set_ylabel('Position: w')

If :math;´a_1´ is positive then the process oscilates backwards and forwards.

fig,axs=plt.subplots(3,3)

steps=30

a_vals = [0.9]

for axsr in axs:

for j,ax in enumerate(axsr):

w=AR([0],steps,a_vals)

plotOverTime(ax, w)

if j==0:

ax.set_ylabel('Position: w')

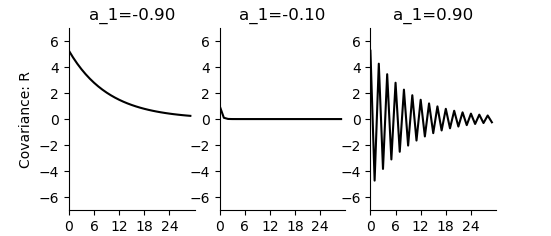

Theoretical covariance

The covariance functionfor AR(1) is calcuated as follows.

def R_theoretical(a_vals,maxtau,sigma=1):

R = np.zeros(maxtau)

for tau in range(maxtau):

R[tau] = np.power(-a_vals[0],tau)* (np.power(sigma,2)/(1-np.power(a_vals[0],2)))

return R

rcParams['figure.figsize'] = 14/2.54, 6/2.54

fig,axs=plt.subplots(1,3)

for i,avals in enumerate([[-0.9],[-0.1],[0.9]]):

ax=axs[i]

if (i==0):

ax.set_ylabel('Covariance: R')

txt='a_1=%.2f'%avals[0]

ax.set_title(txt)

R=R_theoretical(avals,maxtau=steps)

plotOverTime(ax, R)

ax.set_yticks(np.arange(-10,10,step=2))

ax.set_ylim(-7,7)

plt.show()

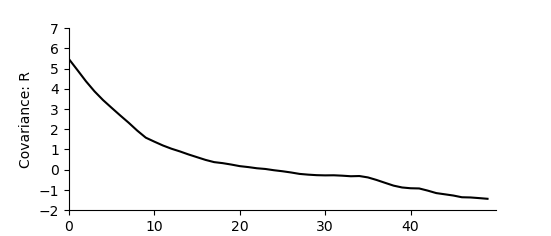

Empirical covariance

Fill in the code below to write a function yourself to calculate the empirical covariance.

Then use it to calculate the standard deviation over 1000 time steps of an AR(1) model with :math:´a_1=-0.9´.

def R_empirical(w,maxtau):

steps=len(w)

R = np.zeros(maxtau)

for tau in range(maxtau):

Rk = np.zeros(steps)

for k,wk in enumerate(w):

if k<steps-tau:

Rk[k] = w[k+tau]*w[k]

R[tau] = np.sum(Rk)/(steps-tau)

return R

fig,ax=plt.subplots(1)

ax.set_ylabel('Covariance: R')

a_vals = [-0.9]

steps=1000

w=AR([0],steps,a_vals)

R=R_empirical(w,maxtau=50)

plotOverTime(ax, R)

ax.set_yticks(np.arange(-10,10,step=1))

ax.set_ylim(-2,7)

plt.show()

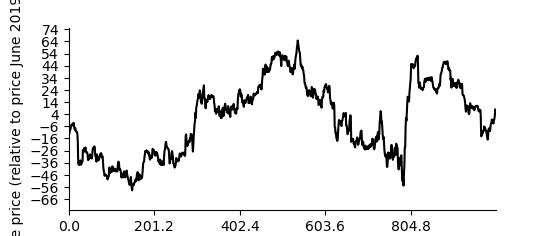

Share prices

Now let’s use your function to calulate a covariance function for H&M share prices. First lets load in and plot the data.

import pandas as pd

share_prices=pd.read_csv('../data/HandM.csv')

w = share_prices['Average price']

w=np.array(w.dropna())

fig,ax=plt.subplots(1)

w=w-np.mean(w)

plotOverTime(ax, w)

ax.set_ylabel('Share price (relative to price June 2019): w')

ax.set_ylim(-75,75)

plt.show()

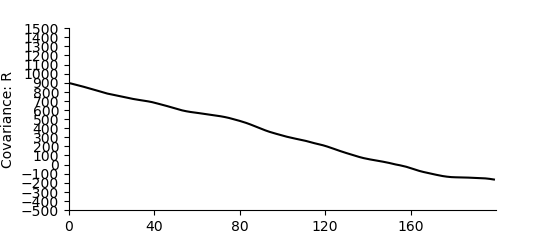

Share prices

Now plot the correlation as a function

fig,ax=plt.subplots(1)

R=R_empirical(w,maxtau=200)

plotOverTime(ax, R)

ax.set_yticks(np.arange(-600,1600,step=100))

ax.set_ylim(-500,1500)

ax.set_ylabel('Covariance: R')

Text(15.369860017497809, 0.5, 'Covariance: R')

Total running time of the script: ( 0 minutes 1.841 seconds)